The Money Monopoly

Written by Paul Siluch

September 18th, 2023

Day Trader

I met a young man wearing a black hooded sweatshirt the other day when I was in line to buy euros for an upcoming trip. We started chatting, and he mentioned he was “in finance.” I asked what area of finance. He hesitated for a moment, and then said, “I’m a day trader. It has a bad name, but it’s nothing illegal,” he added hurriedly.

“Day trading,“ I replied, measuring my words, “can work for a few people. If you’re quick and manage your risks.”

I felt a mixture of admiration and sadness for the young fellow. The battlefield of investors who buy in the morning and sell by market close – day traders – is littered with impoverished corpses. Back around 1986, a 35-year-old opened an account with me. As I found out, he’d been a bus driver, won a medium-sized amount in the lottery, and retired. He was good at math and liked investing, and so decided he would trade his way to a bigger fortune.

The short version of the long story is that he had early success, but as his confidence grew, his timeframe shortened. He traded more and more volatile stocks and ventured into options trading, which are even riskier derivatives of stocks that have expiry dates. The truth is, your returns are inversely proportional to the amount you trade, and he was trading more and more. He left me because I couldn’t work just for him. Wherever he went, he lost all of his lottery winnings and more. Last I heard, he was back driving a bus.

Speculative trading is not new. The Netherlands was swept up in tulip bulbs, and Jesse Livermore became famous for shorting the market before the Crash of 1929, making a $100 million profit. Tulips are now synonymous with investment bubbles, and poor Mr. Livermore filed for bankruptcy in 1934. He eventually took his own life.

The history of most investors trading frequently (and often frantically) to beat the market is not good. There are always bigger and richer fish in your ocean, and they have advantages you, as a small fish, don’t have. Nathan Rothschild used a system of fast ships, horses, and carrier pigeons to bring him the news of Napoleon’s defeat at Waterloo. Trading on the news a day before anyone else, he doubled the Rothschild fortune.

In the last two decades, trading firms and hedge funds have laid fibre-optic cables to outrun older copper wire connections when entering trades. Some have even rented space right beside the stock exchanges to trade even faster. What’s next? There are already artificial intelligence algorithms being used to read patterns so they can spy on your methods and techniques. They front-run small investors and even institutions.

I didn’t tell all this to my young friend. He was obviously quite bullish on his prospects, and probably wouldn’t want to listen to some dinosaur telling him that his odds were grim. What I did say was that my best investments often take years to play out – even the more speculative ones. Time is the one thing the small investor has on their side. We don’t have to trade in-and-out by the hour if the investment is sound.

The Money Monopoly

As I left the wicket with euro notes in my pocket, I realized such an investment was playing out right in front of me.

The currency exchange store had a notice in the window that it was closing permanently. The reason? Volumes never regained their pre-Covid levels, and they just weren’t profitable any longer. My wife and I have travelled extensively and seen the jammed planes to Europe and the overbooked hotels. If currency exchange volumes were down, it wasn’t because travel is down.

I realized their problem is not in how much we exchange, but in how we exchange. Most travellers now use their credit cards. It is easier for the merchant, safer for the traveller, and even governments encourage it. Several European nations now limit cash transactions to 3,000 euros, and France only allows up to 1,000 euros. Cash payments are frowned on in many places. In Canada, try paying with a $100 bill. Some stores won’t accept them because of counterfeits.

The kings of the credit card world are Mastercard in the #2 slot and Visa in #1. Visa was born in 1958 when Bank of America introduced the BankAmericard. It arrived in Canada in 1968 under the Chargex banner and was followed by MasterCharge in 1973. Chargex became Visa in 1977 and MasterCharge became MasterCard in 1979. By 2020, there were almost 76 million Visa and Mastercard cards issued in Canada (source: DebtCanada). Two for every person.

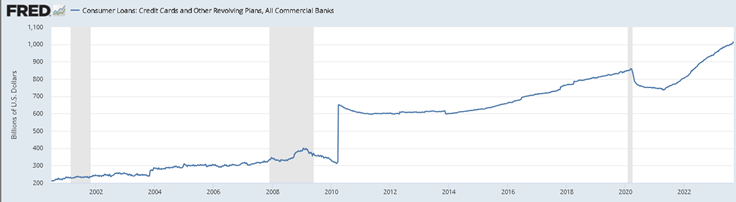

We love credit. Total credit card balances now exceed $1 trillion in the U.S.

Most people think credit cards make money by the exorbitant interest rates they charge, but that is incorrect. Those charges are levied by the banks who issue the cards, and who also assume all the risks of the cardholder defaulting. Visa and Mastercard make their money selling their services to banks, on transaction fees paid by merchants, and on international foreign exchange fees. In 2022, almost 23% of Visa’s gross revenue came from foreign exchange fees – a service once performed by the currency exchange firm now closing its doors.

Our world is increasingly cashless. A Gallup poll found that only 13% of Americans used cash for most purchases in 2022 compared to 28% just five years ago. Norway is down to 3-5% cash transactions, and Sweden claims it is now entirely cashless in its transactions.

If Scandinavians don’t use cash, you can understand why the business of selling cash to tourists travelling to Scandinavia is shutting down.

Visa and Mastercard are like train companies, and their digital payment networks are their rails. No one else has tracks that go as fast to so many places, so they have quite the monopoly. We have owned Visa stock in our Dividend Value portfolios since 2016. The shares have tripled in value in that time, thanks to the rise in people using credit cards and the race to cashless payments. The pandemic was particularly good for the credit card companies, with people stuck at home receiving cash benefits. There wasn’t much to do but order things online.

Do they face risks? Sure. Digital platforms like PayPal and even Bitcoin could replace the legacy credit card networks. Think of what airplanes did to smaller railroads.

Visa isn’t standing still, though. They are one of the biggest users of artificial intelligence to spot fraudulent transactions, and they can now freeze your card in a heartbeat. They are also pursuing digital transactions and are leaders in debit payments as well as credit.

Monopolies aren’t the best thing for consumers. Canada has three large cell-phone providers, and they all charge the same high fees. Same for our two airlines. Monopolies are often good for investors, however, because their moats – what it would cost to replicate and replace them – are usually too large for new players to cross. Companies in such positions tend to be strong and as permanent as any company can be. Warren Buffett loves companies with “wide moats”.

Just like Visa.

Political Noise

Despite rising interest rates, markets have delivered better-than-expected returns this year so far. As it turns out, many companies have been able to withstand higher debt costs because they paid down their debts before rates went up. Many investors are also beneficiaries of rising rates through their savings.

The next year, though, will test even these fortunate ones. High rates may have to go even higher to slow inflation down. Many less fortunate people are suffering from rising credit card debt, higher mortgage payments, and increased taxes.

Meanwhile, we have a U.S. election next year to look forward to.

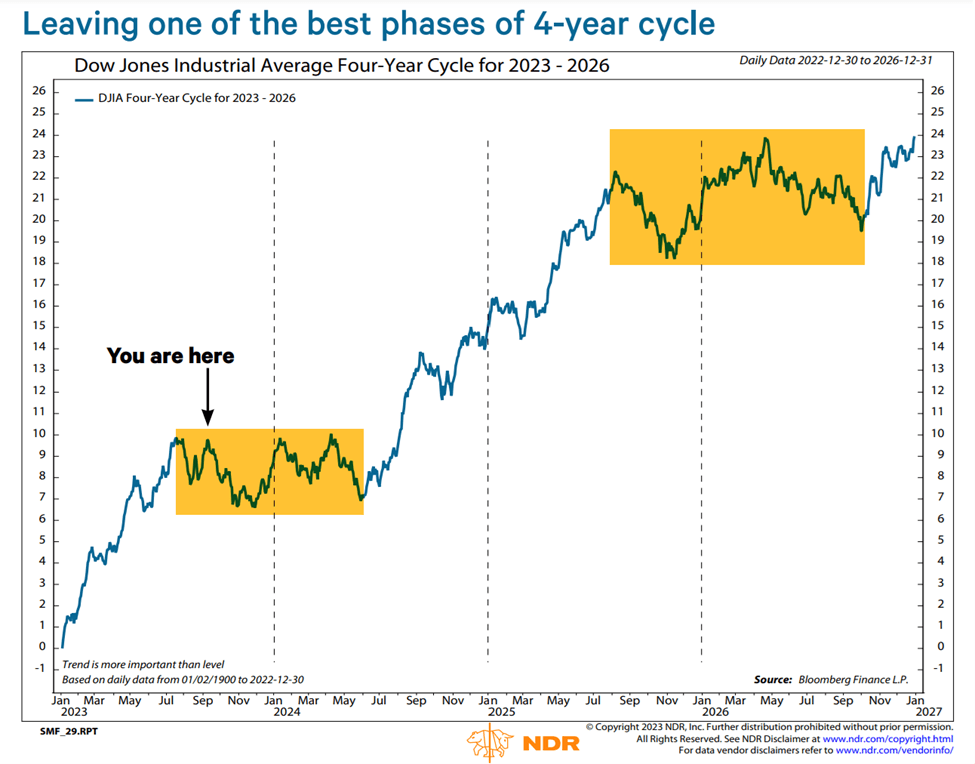

U.S. markets tend to follow certain patterns in the four-year election cycle, as follows:

Year One – The first year of a new president is the Honeymoon year. Markets normally rise, but at the slowest rate of the four-year cycle.

Year Two – The second year is the “bitter medicine” year. Presidents have a full two years before the next election, and so feel safe raising taxes or delivering other unpopular news. Markets are normally flat or down in year two. 2022 – the worst year in recent memory – was a Year Two.

Year Three – The third year of the election cycle marks the beginning of the “get out the sugar bowl” period when tax breaks, subsidies, and other carrots start to be dangled in front of voters. Markets are strongest in Year Three.

Year Four – Many elections are already decided months before voters go to the polls, so markets often rise by mid-year when surveys become more certain. This is the second-best year of the four.

That said, we often have a six-month period when markets churn sideways, starting now. There are a lot of questions about who will be running for president in 2024. Add in foreign wars and interest rate hikes, and this pattern of an up and down grind for the next six months feels about right.

If historical patterns hold, any declines will be an opportunity to invest.

More Babies

The pandemic introduced us to the concept of work-from-home. We couldn’t come into the office because of quarantines, and so tools like Zoom and Teams became enormously useful. They allowed us to teleconference in from anywhere. This was particularly helpful to young mothers who were often the ones most burdened by children kept out of school.

Canada and the U.S. are leaders in allowing work-from-home.

Contrary to public opinion that birthrates might surge with mom and dad stuck at home in 2020, the pandemic accelerated the trend in declining birthrates. If absence makes the heart grow fonder, being cooped up together in a small house did the exact opposite.

However, early surveys from California suggest that birthrates are turning higher. One of the reasons? The freedom that work-from-home offers female workers. They can now maintain a career (or a part-time one) while raising children.

Lower birthrates are a key factor in slowing world growth – just look at China. If working from home by using new technology can help reverse this, the world will be much better off.

![]()