Unreal Estate

Written by Paul Siluch

August 30th, 2023

The word “Hello” is a relatively new word, dating back to just 1827. It was favoured by Thomas Edison to begin conversations on the new invention of the telephone.

Alexander Graham Bell preferred “Ahoy” for his version of the telephone, which was an older Dutch greeting used to greet ships. The first phone book in 1878 included instructions on how to use the device, and the recommendation was to start with a hearty “hulloa,” which made Hello permanent and Ahoy a non-starter.

When your friendly banker calls and says “Hello, your mortgage is coming due,” she is using a much older word.

The word “mortgage” dates back to a French combination from the 1400s. Mort means ‘death’ and gage means ‘pledge,’ so mortgage is, essentially, a death pledge.

Freepik image

At today’s rates, that’s a pretty apt description. Especially if your old rate was 2% and your friendly banker says you are renewing at 6%. That could be a death sentence for many borrowers today.

What Happened, Canada?

In 1988, my wife and I bought our first house for $99,000. We put $10,000 down (every penny we had) and took out an 8% mortgage with a floating rate. I was ‘in the business’ and so knew interest rates had to go down. They didn’t. As rates strangled us, we paid the house off as fast as we could over the next 5 years. Rates peaked at 13%.

No wonder we paid it off quickly.

Housing in 1988 was affordable. You could pay a house down because the average home only cost about three times annual income then.

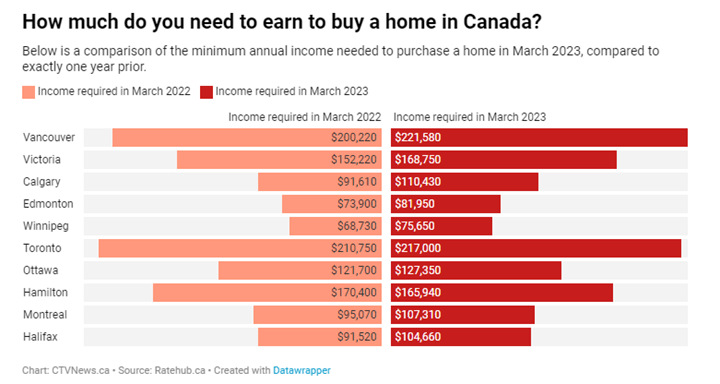

Housing today is ridiculous. The benchmark home price in Victoria today is $1.36 million. New buyers need a 20% downpayment (10% doesn’t cut it anymore) to assume a mortgage of almost $1.1 million. The monthly payments are roughly $6,700 per month after-tax.

CTV News says you need to make approximately $169,000 in income in Victoria to afford a house today. At the median value of $1.36 million, homes cost eight times this level of income. But, the actual average income in Victoria is just $89,000 (source: CMHC). That’s fifteen times the average income, and a giant leap from the three times we first paid.

How did we get here?

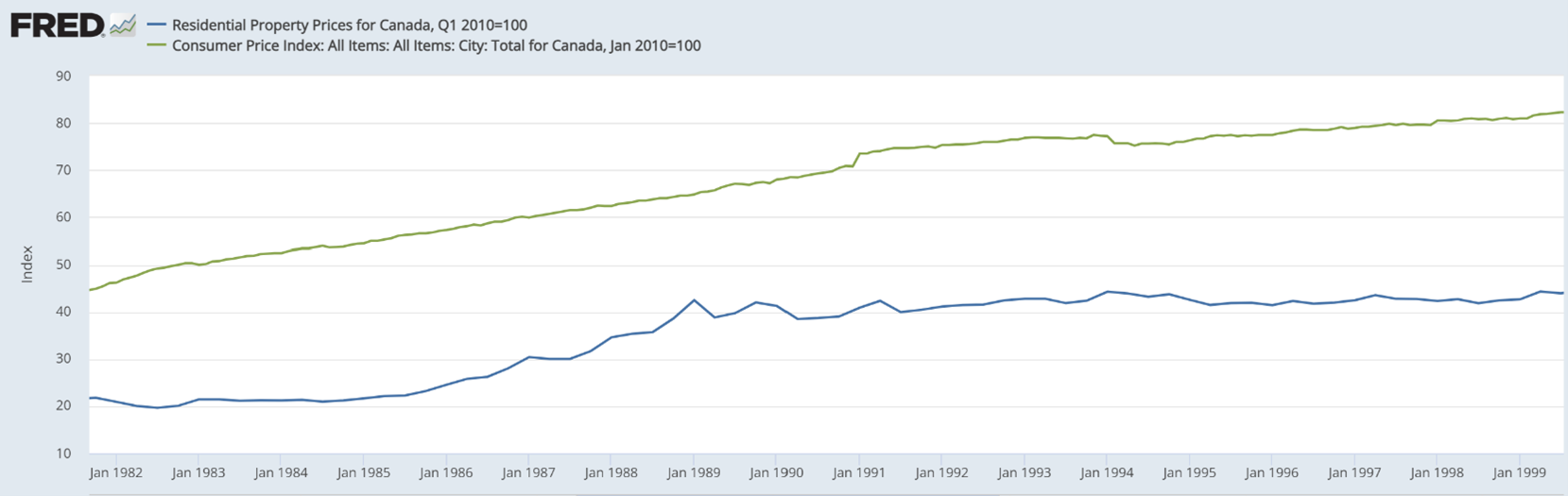

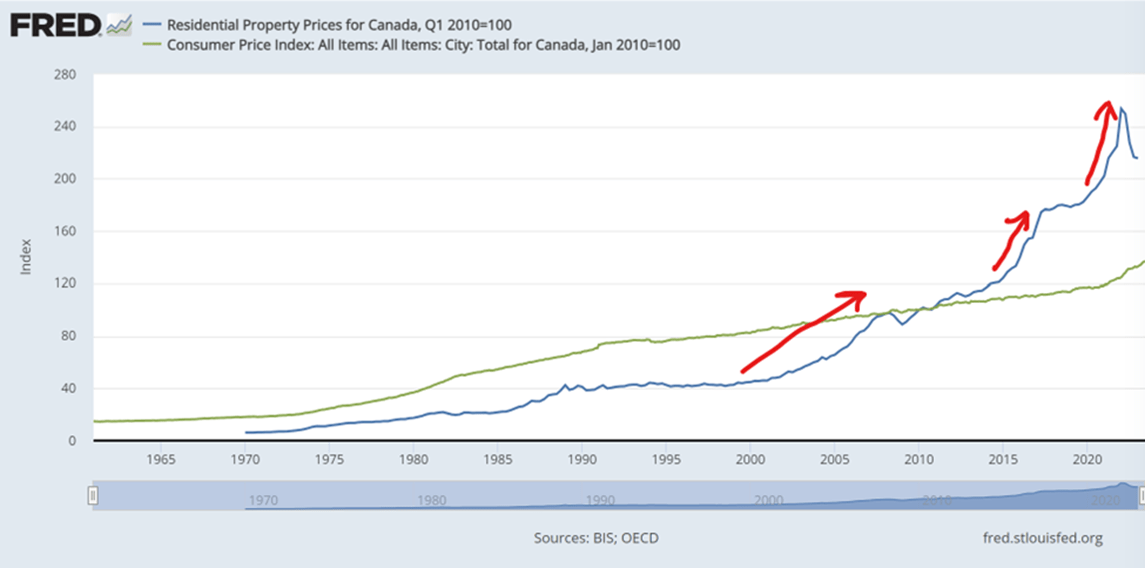

From 1980 to 2000 – after the crazy inflation of the 1970s when home prices tripled in just ten years - Canadian home prices took 20 years to roughly double. That’s not that much in today’s terms, but was in line with inflation, which also doubled.

This makes sense, in that the rising supply of money should equal the rising price of hard assets like real estate.

It wasn’t even. After a quick jump in prices from 1988 to 1990, values stayed flat until about 2002. Interest rates fluctuated in a 4-6% range. Until 2001, that is.

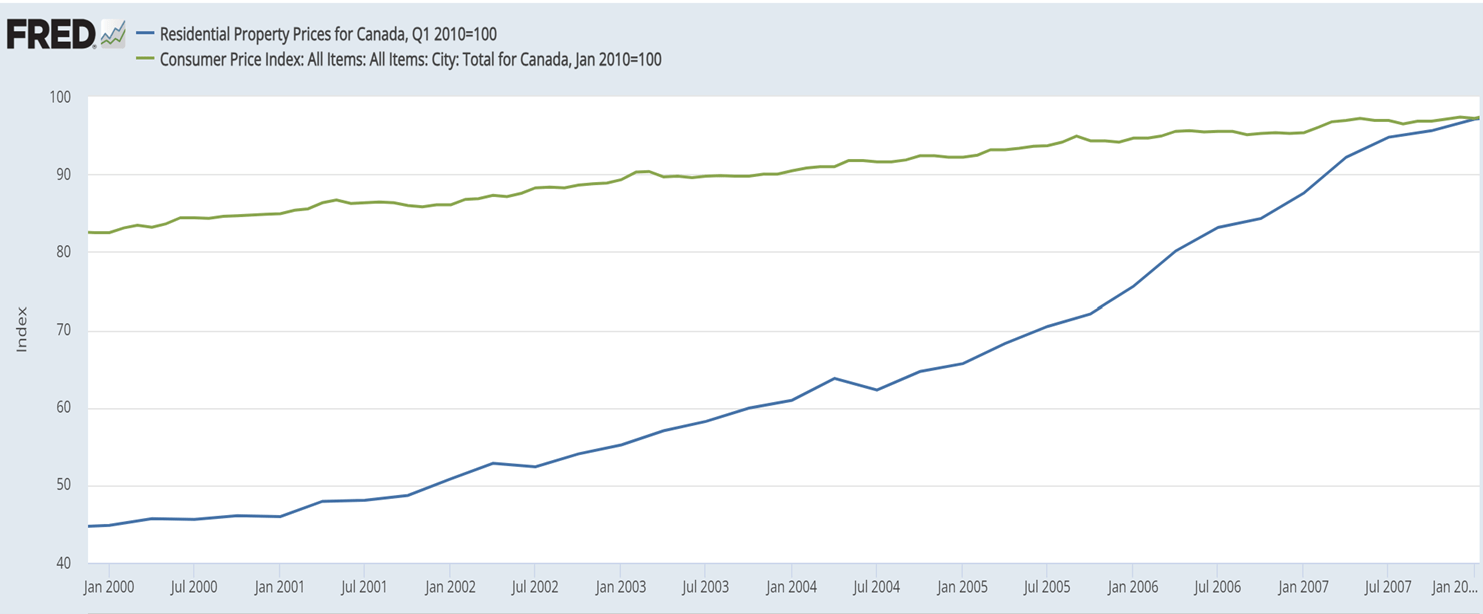

The dot.com crash of 2000 changed everything. When Nortel, Worldcom, and Enron collapsed, and every other technology company was cut in half (at least), rates were slashed to reinvigorate the job market. This is the magic tool central bankers use whenever they need to prime the economy.

Canadian real estate surged. Prices doubled from 2000 to 2008, catching back up with inflation completely after lagging behind for most of the 1990s.

Was that it for rising home prices? Not even close.

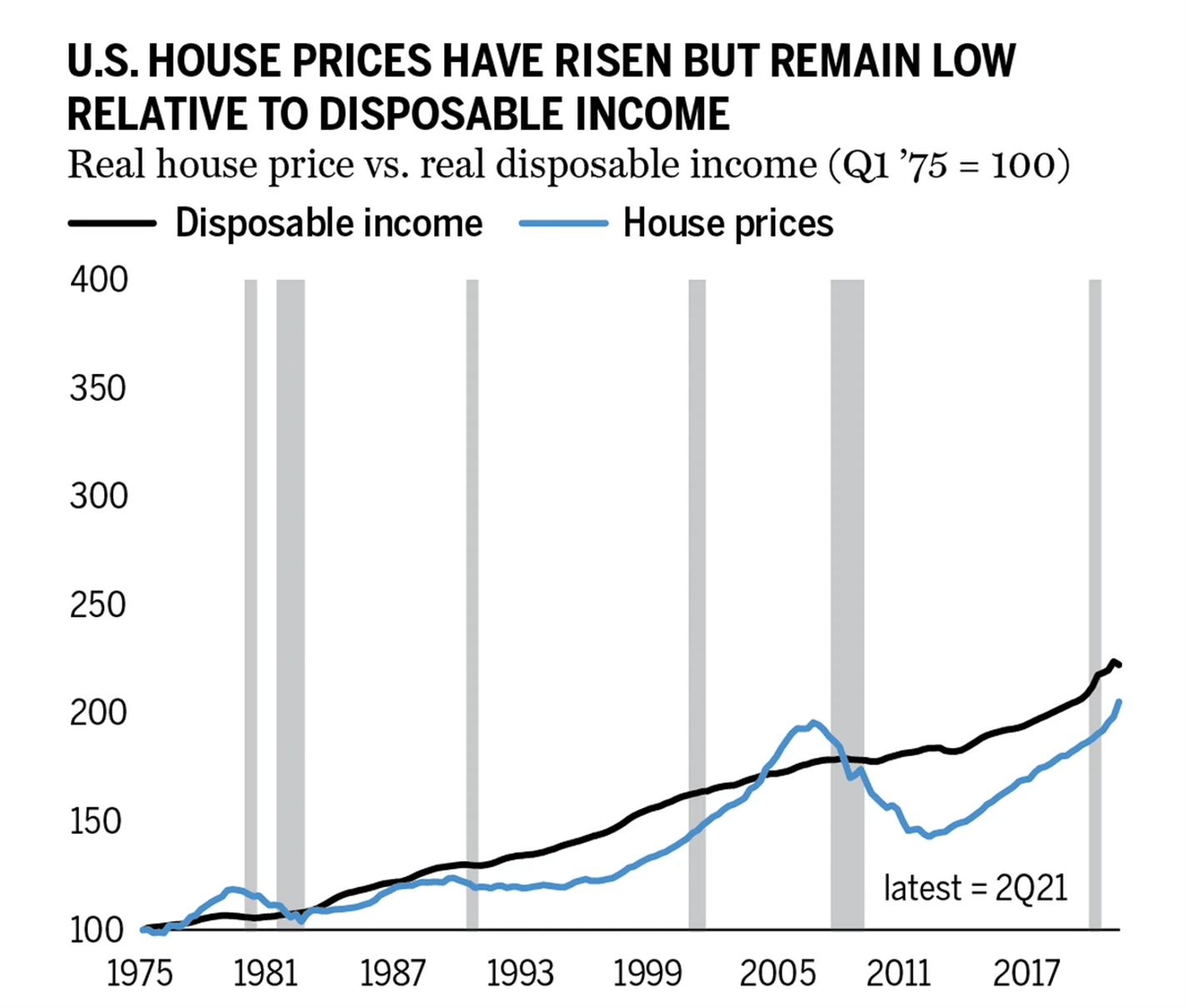

The 2008 Global Financial Crisis saw home prices decline all over the world due to bank failures. Particularly in the United States, where NINJA mortgage loans – No Income, No Job, no Assets - were made to millions of people. These loans defaulted and home prices cratered.

Once again, in 2008 the magic tool appeared to lower interest rates. All the way to zero this time. House prices in the U.S. fell in the beginning with all the defaults, then rose as new buyers were enticed by all the bargains.

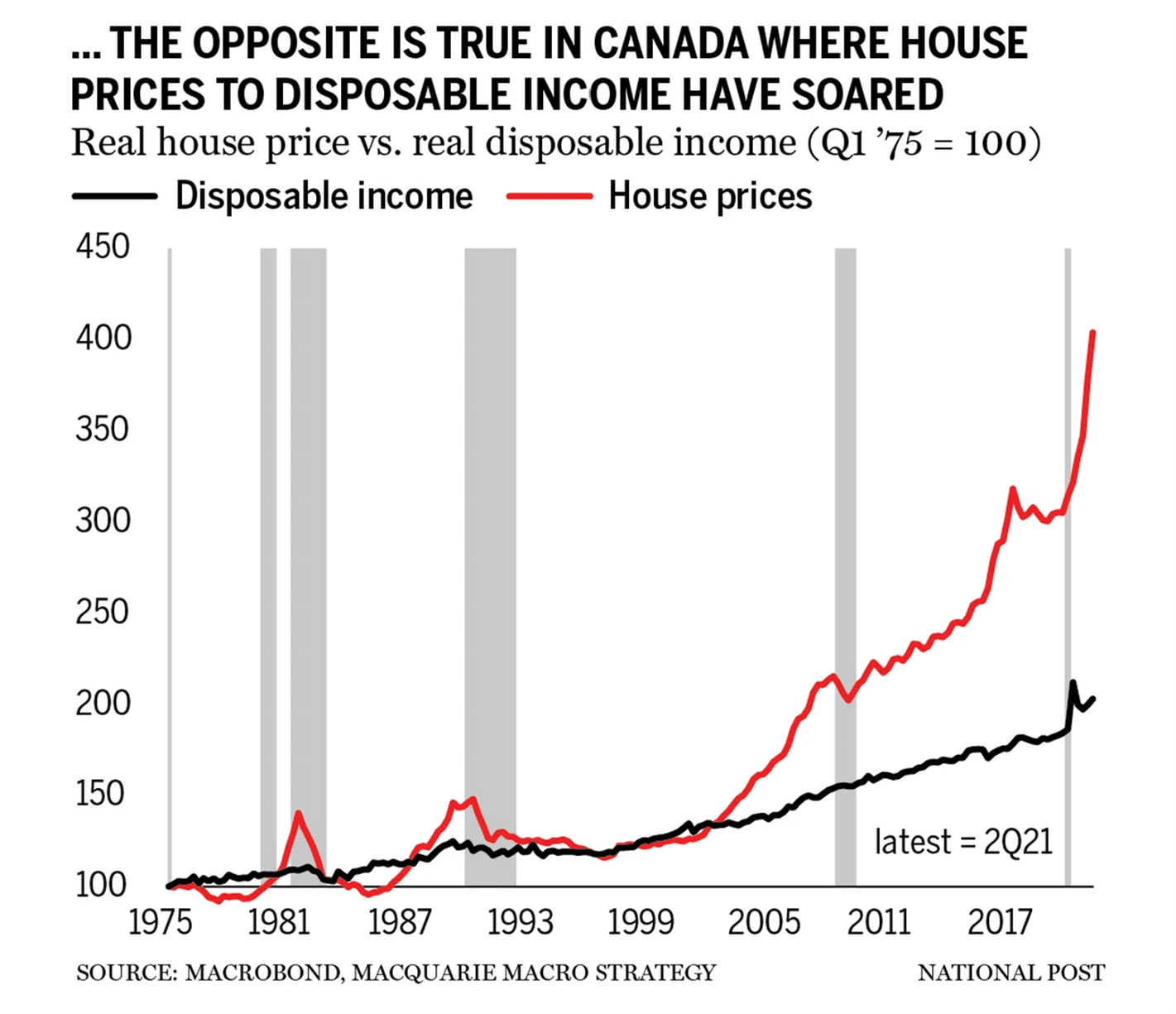

Source: MacQuarrie, Financial Post

We did not experience this in Canada - no bargains showed up for us. Our solid, stodgy, conservative banking sector became a blessing and a curse. Our banks had lent only to buyers with income, jobs, and assets. We didn’t see the same default rate as the U.S. did, so new buyers just kept paying higher and higher prices.

It was a huge blessing for existing homeowners. Ultra-low rates cut mortgages to near 1.5%, which sent real estate prices flying higher.

Canadian house prices rose 80% from 2008 to 2020 while inflation rose just 15%:

But wait, there’s more…

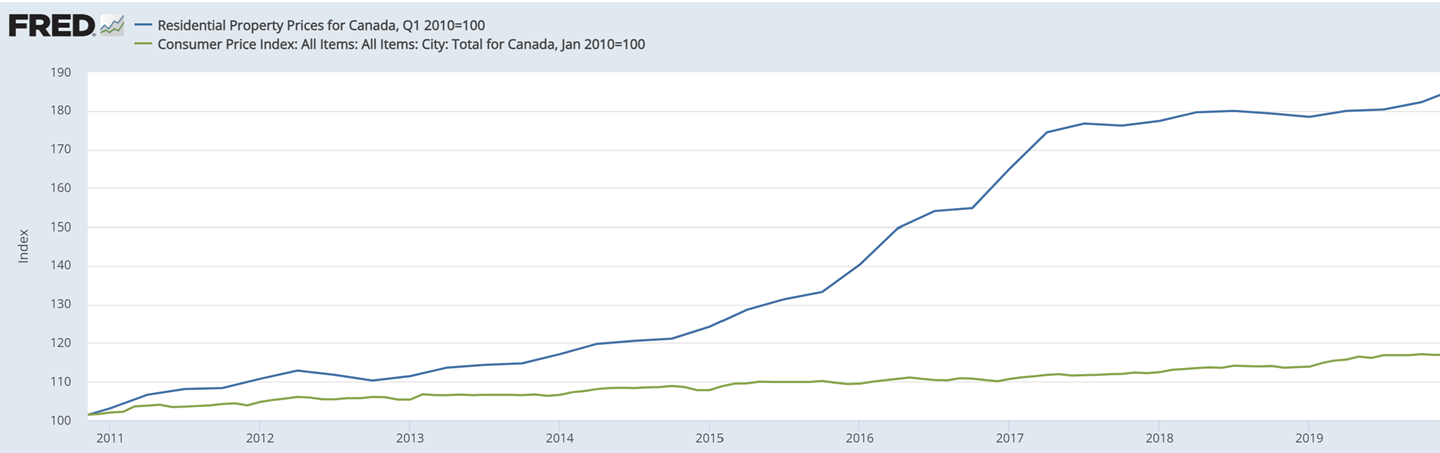

Canada’s central bank recognized the problem in 2017: house prices were growing faster than incomes. They began hiking interest rates. This continued until something called the Pandemic came along in 2020.

Cue the magic tool once again – the cure-all for everything. Interest rates were slashed to zero once again, and trillions more in stimulus payments were mailed out worldwide.

Real estate prices responded the same as they had in 2009 and went up exponentially, adding another 50% to homes in just one year:

Again, this was GREAT for existing homeowners. And, it fired up animal spirits in those who didn’t own a home.

Get in now, or you never will! New buyers piled in.

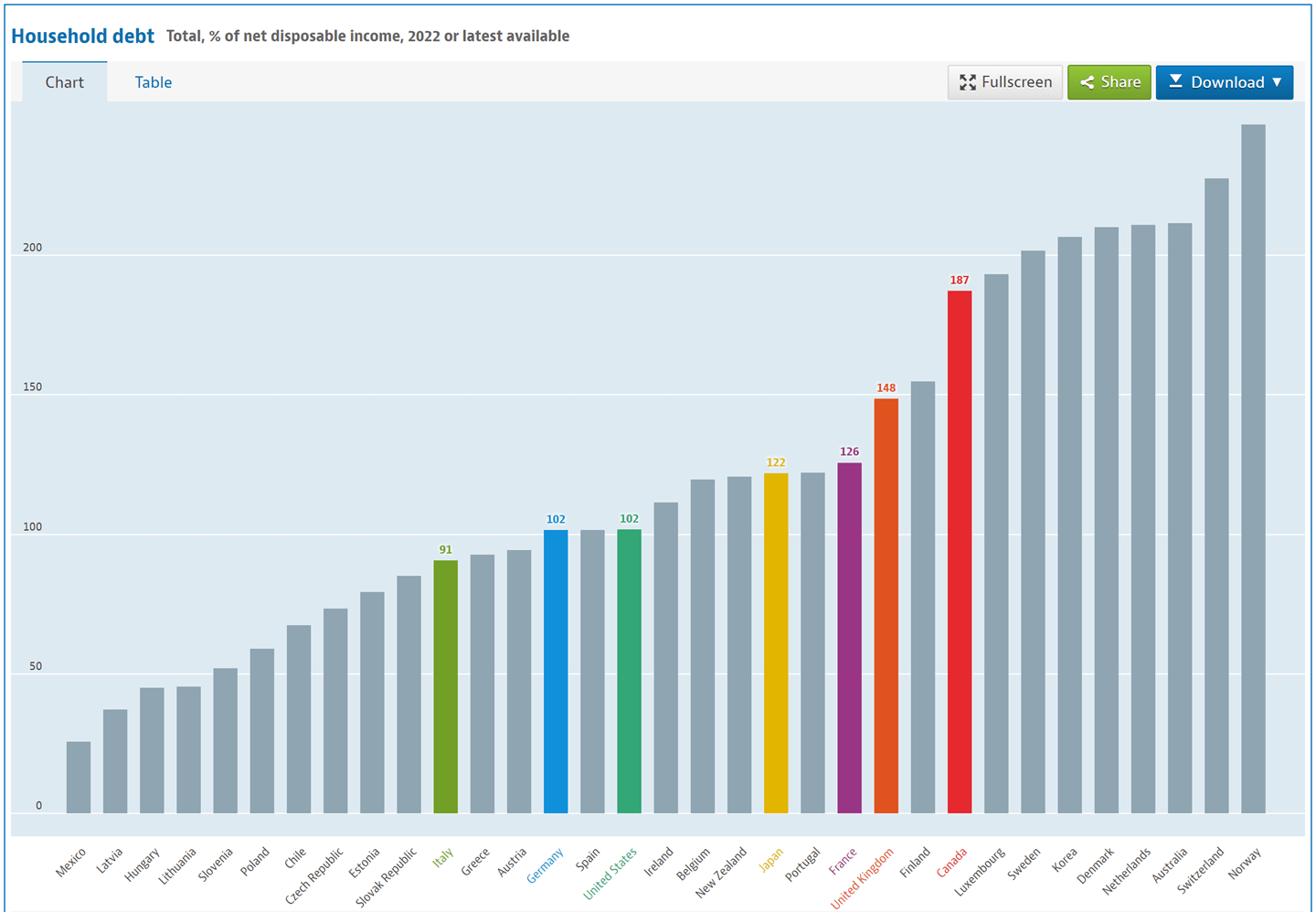

Canada’s conservative banks don’t lend NINJA-type loans. However, we have our own version of sub-prime lending, which includes things such as loans for down payments, extended amortization up to 35 years (now 43% of new mortgages), variable rates, and lowered debt service ratio allowances.

As a result, Canadians have become some of the biggest borrowers on the planet in terms of household debt:

Source: OECD Data

Hidden Risks

Close to 50% of all new mortgages signed from 2020 to 2021 have variable rates - rates that immediately rise with T-Bill rates. About 25% of Canadian mortgages today are variable rate (source: cbc.com). When interest rates were below 2%, as they were then, borrowing short-term seemed like a no-brainer.

These homeowners are feeling the sting of higher rates as 2% is now almost 7%.

And the other 75% hiding in fixed rate mortgages?

Unlike U.S. banks that offer 30-year term mortgages, Canada’s banks only lend for 5-year terms. This means by 2026, nearly all mortgage holders will see their payments increase unless rates fall sharply.

“The typical mortgage payment will be about 20 per cent higher over the next three years,” says the CBC article.

What Happens Next?

To recap:

- Canadian real estate prices are abnormally high.

- The US experienced a crash after 2008 that reset values lower so new buyers could afford a home. Mortgages defaulted, which cleared the deck for new future borrowing. Canada did not experience any of this.

- Higher rates mean monthly mortgage payments are soaring. Homeowners are pulling cash out of Canadian retirement savings to fund these higher payments.

- Higher rates may be around for longer than we think.

The average home price in Victoria today is $1.36 million. The average income in Victoria before taxes is $89,000. How many people can afford a home worth fifteen times what they make, before taxes?

Not many.

Clearly, the trend is unsustainable. There are three scenarios that could happen.

- The first is a hard landing. This would be a housing crash like that of the U.S. in 2008 when prices fell 50%. Such a decline would put houses more in line with historic ratios. But it would also be a very painful way to resolve things.

- The second scenario is a soft landing. This would see house prices stay flat for a decade – like what we saw from 1990 through 2002 - while incomes increase and immigration continues to surge, bringing in new buyers. How likely is this? Central banks always aim for soft landings, but rarely achieve them.

- The third, and most realistic, scenario is something between a hard and soft landing: a modest correction in prices even as inflation and incomes rise. We saw this from 1980 to 1982 when nationwide house prices fell 10% and then flatlined for another four years. Inflation slowed and interest rates fell, which helped affordability. Don’t forget all the strikes going on today. This is good for average wages, making homes more affordable.

The gap between home prices and income has never been this wide, which suggests a correction in house prices lies ahead, alongside a continued rise in inflation. Much depends on interest rates. Our central bank is determined to keep rates high to lower inflation, and yet even the government is struggling to pay the interest on its debt with rates where they are.

“Higher for longer” is a phrase we hear more and more, even as there are calls for cuts to bring relief.

Will politicians be able to resist bringing out the magic tool once again, and cut interest rates to stimulate a weak economy? History suggests they will. The problem is, the magic tool has been used so much, it may not work as well this time around.

Meanwhile, the savings and investment industry (us) can look forward to a few more years of capital outflows as money is diverted to rising mortgage payments instead of retirement savings. Paying more for a non-revenue producing asset while saving less for retirement is a terrible formula for future prosperity, but that is where the policy of continually juicing the real estate market through low rates has brought us.

Markets This Week

U.S. markets are down about 2% in August so far, and Canada’s S&P/TSX is down a more modest 1%. The months of August through October can be rocky for stocks, so this summer has been mild compared to other years.

Bad news is good news right now. We’ve seen new home starts, employment, and retail sales all slow down, which means our central banks may pause their interest rate hikes. Canada’s central bank makes its next rate announcement on September 6th and the U.S. on the 20th. Will the news be bad enough to delay further hikes, but good enough that we don’t slide into recession?

That is the knife-edge bankers are walking right now.

![]()