2025 – An Interesting Year and Number

Written by Paul Siluch

January 3rd, 2025

2025 is an interesting number.

Note that I said “number” and not “year.”

The digits add up to 9 as follows: 2 + 0 + 2 + 5 = 9. Any number that adds up to 9 or a multiple of 9 will evenly divide it. This means the number 2025 evenly divides 9 by 225. The same works for 3 and 6. It is a pattern some people discover intuitively while many don’t.

The number 9 is special to many cultures. It is considered lucky in China; the king of the single digit numbers signifying completion in numerology and has special relevance in all parts of culture. There are nine planets, for example, and it takes nine months to gestate a baby.

2025 is also a perfect square: 45 x 45 = 2025. This is rare in that only 1849 (43 x 43) and 1936 (44 x 44) occur in the last two centuries.

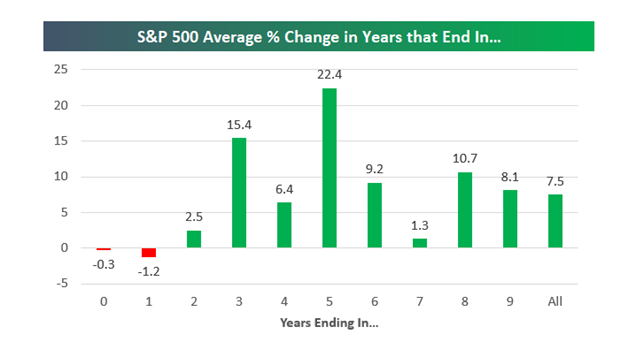

Source: Bespoke, S&P500 data to 2018

Years ending in 5 are also special in the stock market. Going back to 1927, mid-decade years have performed better than every other year:

Pattern Finding

Humans look for patterns and are good at it. We needed this skill to recognize where to hunt and how to avoid becoming hunted ourselves.

Artificial Intelligence, or AI, is even better at pattern finding than we are, and this is the basis of the current boom in Deep Leaning, Neural Networks, and all the terms we associate with AI today.

It may also be key to market returns this year. So much of 2024’s return – at least in U.S. markets – was built on the huge returns of just seven stocks we call the Magnificent Seven.

Each of these giants - Tesla, Microsoft, Amazon, Alphabet Google), Meta (Facebook), Apple, and Nvidia – have benefitted from the halo of being a leader in the AI race.

Let’s go back to the number 9 for a minute. I discovered that nine is divisible into numbers whose digits add up to nine (18, 27, 36, for example) when I was about ten years old. An AI program would have picked this up in seconds, if asked. It is why they are so ground-breaking in such fields as protein folding, which involves billions of combinations and patterns, and writing in plain English, because they can identify the patterns in which humans write and then copy them.

Because of this, we have bestowed rich valuations on the “Mag 7 “ stocks because AI is sure to keep delivering productivity miracles. More companies are finding ways to use AI to speed things up and lower costs than ever before.

It will never end, right?

For the boom to continue, AI needs to keep surprising us. The problem is the surprises are slowing.

For example, to find patterns, these programs need more data to search out patterns. However, we are running out of fresh data for them to scan. No new data means fewer improvements on the patterns they can find.

And more importantly, it may be that this version of AI is a dead end in terms of true sentience. An AI program, for example, needs to scan thousands of pictures of a cat to recognize a feline in any light, pose, or picture. A child just needs to see one cat to recognize a second one.

Sentient mammals can also stop and say “hold on a second” if things don’t feel right.

Perhaps this is related to our survival drive, but whatever it is, AI programs struggle to stop when things are going wrong.

It may mean that pattern matching is a key to true intelligence, but not necessarily the way to get there.

Either way, we are seeing tremendous productivity increases from the new AI systems. However, we have built up high expectations for all of these stocks. If the gains are not as good as hoped, then these stocks could suffer.

We also need to see a ‘killer program’ like YouTube, Instagram, or Spotify to commercialize AI and make it profitable. It took years after the dot.com boom for these ones to appear. We could be waiting for several years before one for AI shows up.

Santa Blahs

December was a weak month for stocks. The year definitely did not end as strong as 2024 started out.

Blame it on recency bias.

Recency bias is when we give greater importance to what just happened recently versus long-term trends. Like thinking Christmas cheer will last through the winter. Fat chance. We’ll be hitting the January blues by next week as the trees and lights come down, and the bills come due.

Recency bias was a useful trait when viewed on a hereditary basis. If you were a neanderthal nomad and a tiger attacked you, for example, you would look out for tigers everywhere for weeks. Since it was probably stalking you, watching your back was smart behaviour.

It doesn’t translate as well to complex systems and modern markets, however.

Insurance rates go up after major rainstorms to cover losses, but also because flood experts become more fearful today of heavy rain tomorrow because of yesterday. Yet the clouds are now empty!

The stock market is an even better example of recency bias. I went back and re-read a letter I wrote to clients in March of 2009, right at the market bottom. Almost 75% of investors in the American Association of Individual Investors (AAII) were bearish at the bottom, right before one of the biggest rallies in history and the start of the 15-year bull market.

When markets are down, investors get gloomy. And they expect things to get worse. Look at several recent market bottoms:

- 74% of individual investors expected things to get worse in 2015 when markets fell about 14%. Markets subsequently rallied +16%.

- Sentiment became even more morose in early 2016 when the Dow Jones Industrial Average dropped -13% in just three weeks. Almost 77% of all individual investors believed markets would get worse. Instead, stocks rose +28% by year-end.

- The lowest bearish sentiment got was 78% in October of 2022, after markets had declined -20%. What happened going forward? Markets pushed higher by +30% just 14 months later.

The converse is also true. Good cheer mirrors what the stock market has done.

We can get too giddy, though. Any reading from the AAII over 50% bullish often signals a top. We saw a high reading of 52.7% bullish in mid-July, which preceded a -7% decline and struggling markets for two months. Markets then rallied from September through November, and sentiment reached 50% bullish again.

While Santa came to visit the kids this year, he missed Wall Street. The seven-day period from December 25th through January 2nd is known as the Santa Claus Rally because markets rise almost 80% of the time with an average gain of +1.3% (Reuters). Perhaps because we were too optimistic in November, markets were down in December – especially in the Santa Rally week.

We don’t always get everything we want for Christmas.

Predictions and Forecasts

This is the time of year when analysts and economists write Prediction and Forecast letters. Most don’t get it right. Only two US analysts out of hundreds in December 2023 forecast gains of 9% for 2024 last year (source: Bloomberg). The S&P 500 blew past this in March on its way to 20%.

So, I will avoid predictions. However, there are two main areas to think about for the year ahead: the economy and valuations.

The Economy

How strong is our economy? Canada may already be in recession…we just don’t know it yet. Our unemployment rate of 6.8% (Bank of Canada) is the highest in 8 years if you exclude the momentary blip of the pandemic. A recent CIBC poll said paying down debt is the top financial priority for Canadians.

Unemployment is the U.S. is just 4.2% (Bureau of Labor Statistics) - a far cry from recession. But 2024 job gains were revised lower by 818,000 jobs (Philadelphia Federal Reserve) so there is weakness out there, even in the USA.

Interest rate cuts are likely to continue worldwide, as a result. They just may not happen as fast as some hope. Inflation is a persistent problem (bought meat lately?) which tends to keep interest rates higher than they would normally be.

Canada is still on track to cut rates more than the US, which means the Canadian dollar could dip further. It is inexpensive already, so don’t expect a dramatic decline from here. Expect exports and tourism inflows to surge.

The big question is this: is Canada too cheap to ignore now?

Valuations

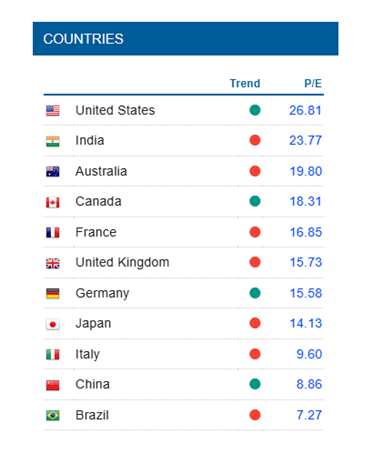

Because just 10 stocks out of 500 in the S&P 500 constitute 37% of its weight. Their high valuations mean the overall US market is the most expensive in the world. This premium is justified, in terms of growth, but things move in cycles. The US won’t always be on top.

Worldperatio.com

When you start from an expensive point, forward returns for US indexes are likely to be low.

JPMorgan plots monthly data from 1988 and shows high valuations today result in low returns going forward. Forward returns over the next 10 years show returns of just 3-5% per year, on average.

It has never been more important to diversify globally.

An Average Prediction

The S&P 500 has delivered an average annual return of 10.13% since 1957 (Investopedia). Jeremy Siegel, the American economist, predicts 2025 will deliver 0-10% - what almost every economist says every year.

You can’t go wrong predicting average!

- Siegel expects broader market gains in 2025 to be more modest than 2023 or 2024, with the S&P 500 likely delivering returns in the 0-10% range.

- A dip can’t be ruled out. Growth sectors may face headwinds from rising rates, and a case can be made where they are down 10%.

- Small-cap and value stocks, especially those tied to domestic production, could see a relative boost and have returns from 5-15%.

- However, all 12-month predictions come with a large standard error.

Knowledge at Wharton

To sum up,

- Years ending in 5 are the best of the decade, historically.

- Investors are gloomy for 2025. Bad sentiment means selling has been heavy and money is waiting on the sidelines.

- Valuations in the U.S. are high, but only in a few stocks. Global valuations, including Canada’s, are more attractive.

Here’s to 2025 being another an interesting year.

![]()