A Nickel Ain't Worth a Dime Anymore.

Written by Paul Siluch

November 6th, 2024

A Nickel Ain't Worth a Dime Anymore.

- Yogi Berra

The Timelessness of Economic Trends

Every generation thinks it invented sex. That’s what my grandmother said, and she was a wise old girl. If you doubt it, have a look at the frisky mosaics in Pompeii, or the Greek statues from Athens, circa 475 B.C.

We may think of ourselves as daring and inventive, but there is nothing new under the sun when it comes to creating more humans.

The same present-day blindness we apply to sex also applies to monetary policy. We think everything we do is new, but it isn’t. Alan Greenspan lowered interest rates in 1987 to soften the pain of the October Crash and, ever since, we have been manipulating rates to zero and below. We buy bonds to goose the economy. We print money to force rates below zero.

Buying bonds? Negative interest rates? Never been done before. Except both have.

- The Genoans pushed rates from 9% to 1.1% in the 1500s.

- The Dutch did the same a century later. This made them more competitive for a time, until too many bad investments led to decline.

- From 1789 to 1796, the French printed assignat bonds faster and faster as they devalued, until the currency system collapsed in 1796.

(Visual Capitalist)

Both the U.S. and Canada forced interest rates to almost zero during the 2000-2002 recession and the 2008 financial panic. Then, we printed money in the 2020 pandemic crisis. Both helped our economies recover. But at what cost?

What is inflation?

Inflation is the price increase in the stuff we buy. If stuff costs 8% more in 2023 than 2022, then inflation is 8%.

Inflation has stayed quiet for two decades, making us think we fooled mother nature. Until we didn’t. Inflation rocketed to 8% in 2022 after the pandemic and is only now subsiding. Lingering inflation may decide both the U.S. and Canadian elections in 2024 and 2025.

How does inflation occur? When money becomes worth less – such as when we print more of it – it means what we buy costs more.

- The Romans discovered this when they cut the silver in their denarius silver coins.

- The Germans printed billions of marks (the papiermark) in 1921.

To reduce prices, deflation is needed, which typically follows a severe recession—something most people want to avoid.

Current Inflation Trends

As of September 2024, Statistics Canada reported annualized inflation of just 1.6%. This is a big decline from the horrific 8% spike in 2022, so this is welcome news. Most of this drop comes from gasoline prices, so if you have an electric car or take the bus, you might not feel it. Your personal inflation might be higher.

Will inflation stay low? Central bankers hope so. That will enable them to keep interest rates down, which helps home sales and government finances, because governments are such big borrowers now. Rates may be tough to keep down, though. Look at all the strikes for higher wages and tax hikes. Both push inflation higher.

Measuring Inflation

Measuring inflation for a nation is complex, even for the best government scientists. What do you include or exclude? Some important products become obsolete while others are recent inventions. The CPI in 1895 probably included the cost of owning a horse, for example, and computers were added only about thirty years ago.

What they DON’T include is a more relevant question. You’ll see why in a moment when you read what Canadian CPI excludes from its calculations yet still affects all Canadians.

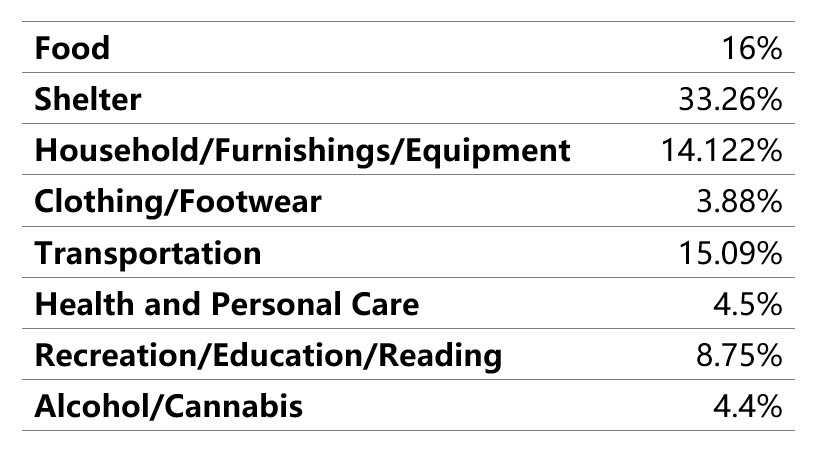

The Canadian Consumer Price Index had these weights as of 2022 (Statistics Canada):

Some categories affect people more than others. If you don’t drink, for example, any price increases in the Alcohol/Cannabis category don’t apply to you. And if you are retired and no longer buy pricey Clothing for business, knock another 4% out of your personal calculation.

Meanwhile, seniors spend disproportionately more on Shelter and Health and Personal Care. Statistics Canada has a ‘Seniors CPI’, so credit to them for recognizing this growing segment of the population. For the record, inflation for seniors is running slightly ahead of the general CPI.

In 2024, the Canadian Realtors Association reported that rents rose 10% across the country. Renters were hit hard. But so were owners. Vancouver city council recently hiked property taxes 7.5% and the City of Victoria is asking for a 12% increase. Rents and taxes get averaged across the country and watered down, so Shelter inflation in British Columbia could be much higher than in other provinces and states.

What CPI Excludes

It is also important to know what CPI excludes. These may surprise you. Here are the biggest exclusions:

- Income taxes – in 2016, the top BC tax rate was 43.7% (Americans, don’t choke). Today, it is 53.5%. That is an increase of 24%, or approximately 3% higher per year over 8 years. This is deemed a transfer and is not captured in the inflation number.

- Tips – When we paid for restaurant in cash, tips averaged around 10%. This crept up to 12-15% until payments became electronic, a trend that accelerated during the pandemic when no one wanted to touch “infected” cash. “Tipflation” became a word as the minimum tip rose to 18% with top tips now touching 25%.

“Digital payment processor Square, now renamed Block, said tips at full-service restaurants jumped 25.3% between Q3 2021 and Q3 2022.”

- Econreporter.com

Some statisticians say tips may be partially captured in surveys of meal costs. Officially, they are not part of the CPI calculation even as they meaningfully add to the cost of every meal away from home.

- Life and disability insurance – It is hard to find data on insurance costs and how they have changed since the pandemic, but we do know life insurance payouts jumped after the virus struck. And thanks to higher real estate costs, people are having to take out larger policies to cover higher home prices. So, if you are required to buy life insurance for your mortgage and it costs twice as much, that is not included in the CPI calculation.

- Credit card interest - These can range from 19.9% to 24.9% (or higher). Canadians are carrying far more debt than Americans are, and credit card debt is ballooning. You could be paying 20+% interest on a growing balance, and yet it is not considered in the inflation calculation.

- Line of credit interest – Mortgage interest is included in CPI but borrowing against your line of credit is not. Same as credit card interest.

The bottom line? Interest rates should trend lower as inflation falls. However, it doesn’t mean food and general living costs will fall – it just means they will rise more slowly.

And since it doesn’t look like income taxes and credit card interest are going down, and ‘tipflation’ is only getting worse, let’s hope the official components – food, shelter, fuel, clothing – decline to keep the overall CPI tame.

Life is expensive, no matter how you measure it!

What Protects You?

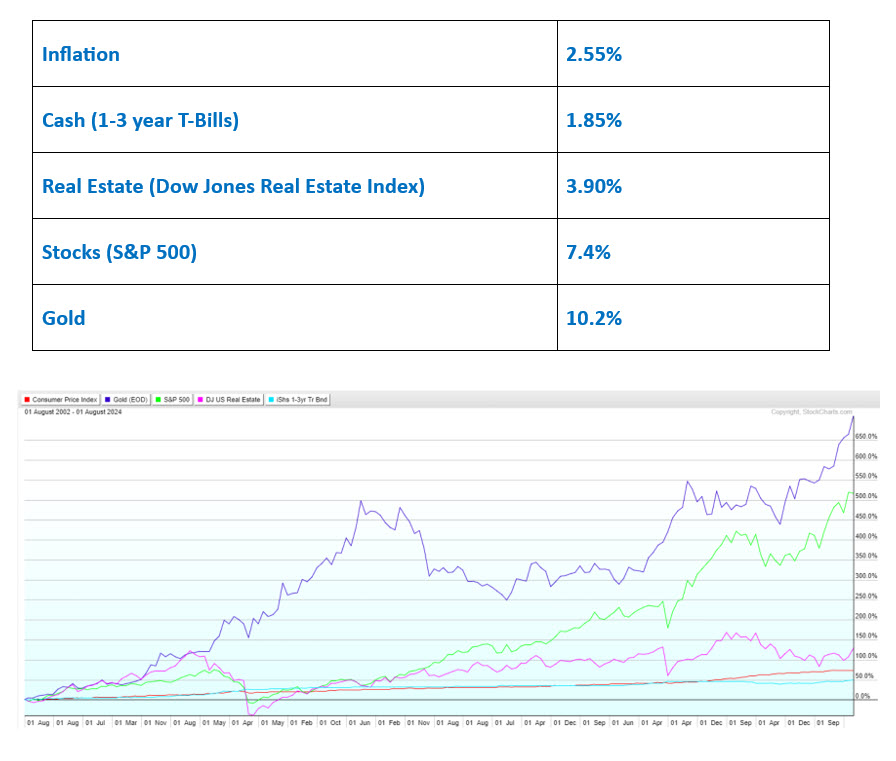

Since the year 2000, inflation measured by the US CPI has averaged 2.55%. In Canada, it is 2.18% (Bank of Canada).

Using the U.S. CPI as a benchmark, what kept you ahead of inflation?

Here are the compound returns going back 22 years (source: Stockcharts):

The Bottom Line?

With deficits continuing in both Canada and the U.S. as far as the eye can see, inflation is likely to be persistent. And it could even get worse.

Real estate, stocks, and gold have been excellent places to hide for the last 20+ years, while cash has lost ground.

Holding some cash is never a bad idea. But over the long haul, people should own assets that rise more than inflation. These are real estate, stocks, and gold.

That is the modern reality.

U.S. Election - First Thoughts

As of Wednesday, the Republicans have control of the Presidency, the Senate, but not the House of Representatives (yet). U.S. markets have responded vigorously.

In no particular order, some points to note:

- Even without control of the House of Representatives, the President can appoint many top positions, such as the head of the Securities and Exchange Commission and the Federal Reserve. These alone could lead to:

- Easier regulations on Bitcoin

- Fewer barriers to companies going public and mergers

- Lower bank capital requirements

All of these reduce the “friction” of doing business – positive for banks and brokers.

- Negatives - Drug stocks are in the Trump crosshairs with RFK jr. in a position to impede pharmaceutical sales. Green power – especially wind – also stands to lose subsidies.

- If fiscal policy (government spending) increases through tax cuts and deficit spending, it may mean fewer interest rate cuts are needed from the Federal Reserve. This is negative for gold this morning, which prefers lower rates.

- Higher spending and persistent deficits are still inflationary, no matter who is in power. Stocks, real estate, and gold eventually do better in such an environment, even as gold and housing stocks are being hurt today.

- Impact on Canada. Our dollar has sunk to U.S. 71.8¢ this morning. Although Trump tariffs are aimed at China, Canada risks becoming collateral damage as companies relocate to the U.S. (and not Canada) to avoid tariffs. Over 70% of Canada’s exports go to America, so we must manage this risk.

(Election Thoughts sourced from Fidelity Canada and Raymond James analysts)

![]()