The Boomers are Selling - What Will That Do to Your Home's Value?

Written by Paul Siluch

August 30, 2024

Most people plan on selling their house when they move into a retirement home. It is a sound strategy, as this is often your biggest asset.

This week, we are going to discuss:

- Why your home went up so much in value

- Why this may be coming to an end

- How to plan for this

We do financial plans for people. The family home is often the largest asset people own and its sale frees up capital in the final years of life to afford ongoing care.

Remember, the final two years of your life are your most expensive in terms of health and housing. Many people need as much home equity as possible.

But will your house be worth what you think it is worth, when you want to sell it?

Baby boomers were once the largest generation ever seen in North America. We were the proverbial pig in the python, pushing prices higher on everything from baby strollers to music sales. About 76 million people were born between 1946 and 1964 in the U.S. (Wikipedia) – approximately four million per year.

Britannica

Canada’s baby boom saw approximately 400,000 born per year from 1946 through 1965 (Canadian Encyclopedia).

Demand for schools skyrocketed – “Los Angeles county opened on average a new elementary, middle, or high school every month from 1946 to 1964” (Britannica).

Demand for teachers exploded commensurately. What was our largest purchase when we grew up, and what did almost every one of us aspire to?

A house.

We became the largest home-owning generation in history.

Click Americana

And we didn’t just stay in our first homes. We bought – and built – bigger ones. Then, we made sure prices stayed high by enacting NIMBY regulations – Not in My Back Yard – to keep others out so we could enjoy our space. Fewer houses on large lots pushed prices even higher.

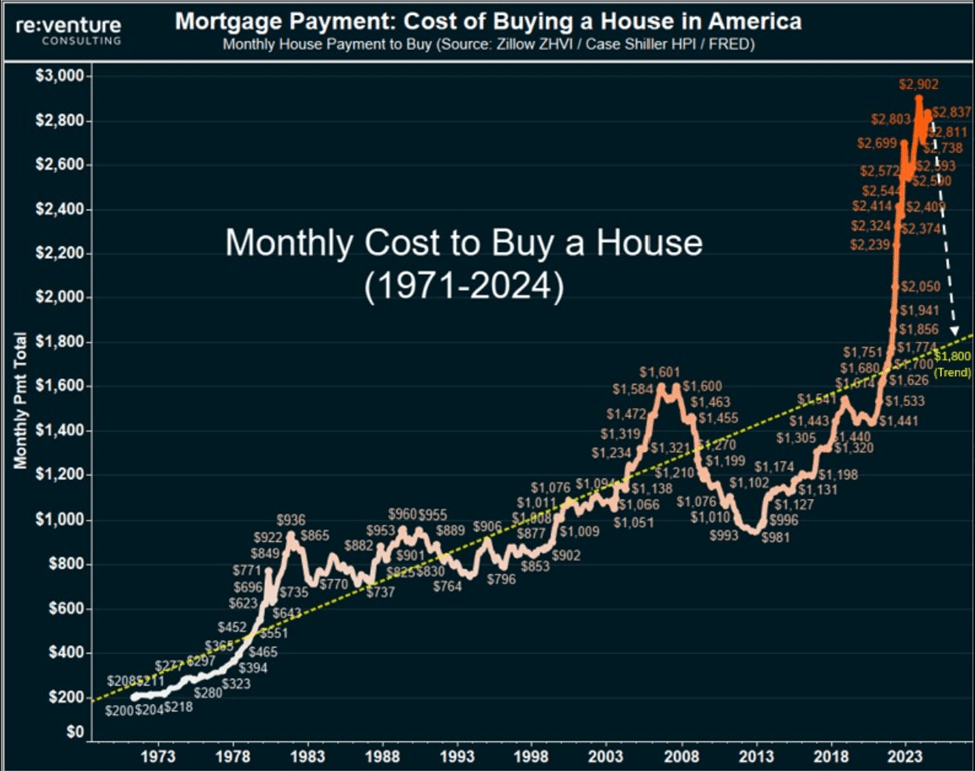

And when a crisis hit? Central bankers – baby boomers, every one of them – lowered interest rates in 2008, when it looked like millions of mortgages would default. Easy credit, limited supply, and a new generation of home buyers called millennials caused prices to skyrocket. In Vancouver, B.C., a home that sold for $200,000 in 1988 reached $1.8 million in 2016 (GlobalNews).

Our homes are now insanely valued and completely unaffordable to the next generation.

Millennials want to own homes, but they can’t afford our homes at our prices. Something has to give. Either their wages go up dramatically (and they may – look at all the strikes) or home prices have to fall more, before houses become affordable.

Millennials don’t have the money to buy a home at today’s prices. The Bank of Mom and Dad can help with the downpayment, which means the next generation’s downpayment is being financed by borrowing against the last generation’s home equity.

That is not sustainable math.

Will All the Baby Boomers Sell at Once?

No. It took almost two decades to make the baby boomer generation, so it may take years to say farewell. But time and tide wait for no one. One of the biggest reasons people sell their homes is stairs. We struggle to go up and down as we age, and they become a hazard.

You may want to “age in place” but gravity has other ideas.

The baby boomer age cohort is now between the ages of 60 and 78, with a median of 69. Approximately 2.1 million die every year (Baby Boomer Death Clock), and this will peak above four million per year by 2050 (Harvard University).

Economists expect most baby boomers will “age out” of their homes between 2030 and 2040 (Syracuse University).

Let’s recap:

- Boomers are the largest home-owning generation, comprising 41.6% of residential real estate wealth in the U.S. worth almost $19 trillion (Syracuse University).

- This is approximately 25 million homes.

- Many will be selling their homes in the next 5-15 years. Zillow estimates an average of one million homes will come for sale per year from 2020 through 2040, with close to four million per year around 2030 (Money Digest).

In 2024, we already see stalled home sales and rising listings. Condo and house sales are down 48% from 2023 levels in Toronto (Building Industry and Land Development Association).

But Wait…

Won’t falling interest rates revive real estate?

Canada has cut rates twice this year and yet home listings are up 22.7% over 2023 (Canadian Real Estate Association). Yes, rate cuts make mortgages more affordable, but central bankers have their hands tied. Lower rates stoke inflation, and they are terrified of that getting out of control.

Lower rates will help, but don’t expect mortgages to fall back to 2%.

As I dug into this article, I realized future home prices are not as clear-cut as this topic first appeared. Why?

- Baby boomers won’t all sell at once. The selling could be more of a steady trickle than a waterfall.

- There is enormous demand for housing today, thanks to pent-up demand and immigration. Canada’s population is double what it was in 1967 and those people need homes.

- We are woefully short of new houses because they are expensive to build due to regulations, rising costs, licenses, and permits.

It is possible that demand for homes will compensate for the sales by the baby boomers. Governments are keen to get people housed, so it all may amount to nothing at all. They may engineer interest rates lower so more can afford large mortgages.

We just have to remember that higher house sales do not necessarily mean higher house prices.

A Prudent Approach

The question for us as financial planners – and you as a retiree – is what to value your home at, when you sell, in some hypothetical future?

Even with many new buyers waiting in the wings, will today’s buyers want our old split levels and monster houses?

“Many homes vacated by aging seniors will not be in demand by tomorrow’s young adults, being in the wrong part of the country or otherwise unsuitable (age restricted communities, for example). Some will be simply too expensive. Some “affordable” vacated homes in desirable locations will be torn down and replaced by larger and more energy efficient / amenity rich houses targeted to older buyers. Many houses will sit on the market for long periods of time before sellers are willing to recognize that they are overpriced. Some homes in declining communities will become abandoned.”

- Joint Center for Housing Studies of Harvard University

I think all of us need to lower expectations for the future value of your home, as well as embed a higher rate of inflation in future scenarios.

Financial plans should consider:

- Reducing the future value of your home by 25% in case all those homes coming to market depress the value just as you are selling. That’s only back to March 2021 prices!

- Model 3% inflation rather than the official 2% target, in case central bankers give up on their inflation fight and cut rates to juice the economy.

If we are wrong, sellers will benefit through more money from a home sale. We may need every penny.

Just as we pushed up demand for bicycles and beer, the eldest baby boomers are already facing long wait-lists for government care. And those lists will get even longer, which means many will be forced into private – and more expensive – retirement care.

Running out of money early is our greatest fear, as financial planners.

If your house is worth more, great. If not, you are prepared.

Hope for the best, but plan for the worst.

Self-Discipline Over IQ

There is an old adage that the A students end up working for the C students.

“The 'C' students run the world.”

- Harry S. Truman

This is because C students work harder to make it. They develop grit - stronger work habits because things don’t come easy.

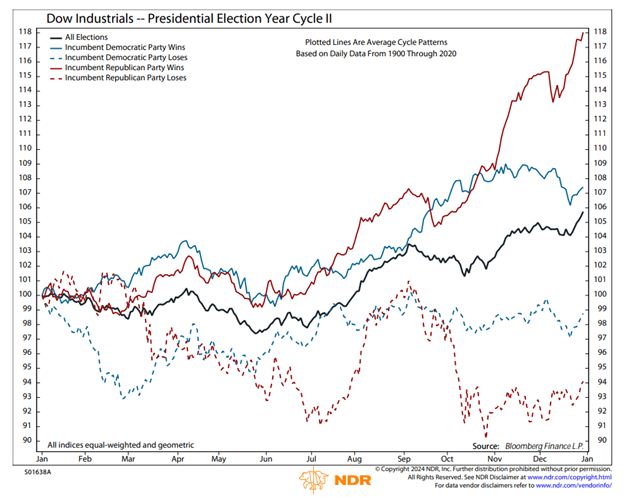

Self-discipline is important as an investor. The chart below breaks down the historic returns of U.S. stocks depending on the political outcome of the election. Some would say it shows you who you should be cheering for in the U.S. election.

The best and worst results are if the incumbent Republicans win or lose. Neither of those can happen this year because the Republicans are not the incumbents.

So, the next best outcome is if the Democrats repeat and win again this November.

What it really says is: markets don’t like change. The devil they know is better than the devil they don’t know.

Either way, the next few months could be volatile. Investors will have to be disciplined if things go sideways.

Here’s how we recommend approaching any uncertain event:

- Stay invested and always own at least a few stocks. Over time, equities have outperformed gold, bonds, and even real estate (Investopedia). And you can’t collect dividends if you don’t own stocks.

- Plan on how you are going to react. Be ready for several outcomes. If your party loses, what will you do?

- Hold some cash aside. There are always opportunities. Especially if there is more chaos than anticipated.

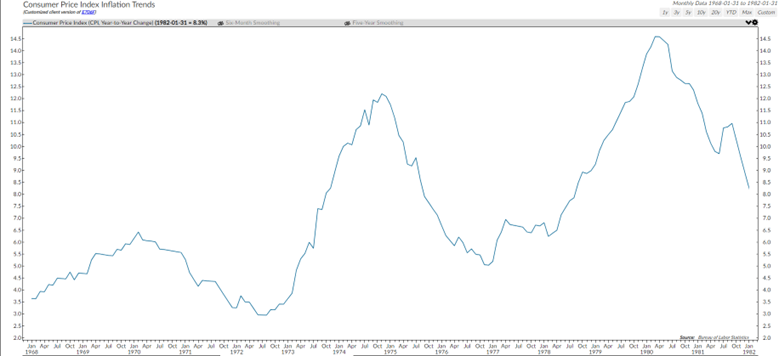

- Inflation is coming – in fact, it is here and isn’t leaving. Inflation can arrive in waves, as it did three times in the 1970s. The U.S. central bank thought they had it licked in 1972 and again in 1977, but it came roaring back each time.

© Copyright 2024 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved.

See NDR Disclaimer at www.ndr.com/copyright.html. For data vendor disclaimers refer to www.ndr.com/vendorinfo/

![]()