Halfway to Halfway

Written by Paul Siluch

July 10th, 2024

Despite 2024 seeming like a brand-new year, the reality is we are already halfway through it. And when we hit 2025, it will be the halfway point of the 2020s. Today is the “Halfway to Halfway” point of the decade.

Halfway is relative, of course:

- Halfway for a mayfly is 12 hours - they live only for a day.

- Halfway for a weasel is 6 months – they live about a year.

- Human ‘halfway’ is 36 years – mankind’s worldwide average is 72 years.

- Halfway for a bowhead whale is 100 years – they can live up to 200 years.

Time doesn’t accelerate, of course, but it sure seems like it. Unless you are a bowhead whale.

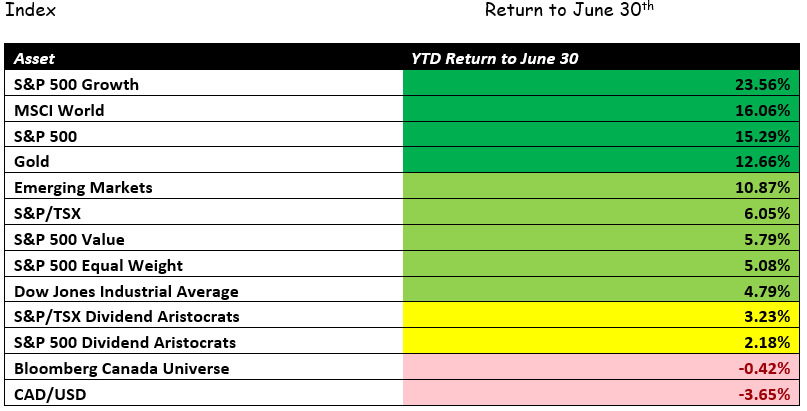

2024 So Far

The winners: S&P 500 Growth, MSCI World, S&P 500, Emerging Markets.

The five largest companies in the world are all technology companies: Microsoft, Apple, Nvidia, Alphabet, and Amazon represent. You had to own at least a few of them to achieve outsized returns so far in 2024.

The S&P 500 Index, its Growth sub-index, and MSCI World own all of them.

Emerging markets are also exposed to technology but through owning Taiwan Semiconductor (which makes chips for AI), Samsung, and several Chinese tech firms.

Mid-Pack: Canada, Value, Equal Weight, Dividends

Most countries and companies were just average this year. Canada is closer to recession than the U.S. and has a much smaller technology sector. We don’t benefit much from AI

Value stocks – industrials, banks, utilities – are suffering from high interest rates and a weak economy outside of AI.

The S&P 500 Equal-Weight Index gives every stock an equal 1/500th weight, which removes the dominance of technology. This index returned just +5.08%.

The Dow Jones Industrial Average, which represents more old-line companies, returned +4.79% to the half year.

The Dividend Aristocrats, which are the giant companies with the longest records of raising dividends, did even worse. In Canada, they returned +3.23% and in the U.S. +2.18%.

The losers: Bonds, Canadian dollar

Bonds returned -0.42% in Canada, and a bit worse in the U.S.

The Canadian Dollar fell -3.65% against the U.S. dollar from January through June. (from $0.7552 to $0.7276).

The S&P 500 index is very unbalanced today. It returned +15.29% because the five top technology companies - Microsoft, Apple, Nvidia, Alphabet, and Amazon - represent 29% of the entire S&P 500 index. This is the largest share since 1964 when AT&T, General Motors, Exxon, IBM, and Texaco were 27% of the index (source: Bianco Research).

When they are weighted equally – every stock in the S&P 500 gets just a 0.2% ‘vote’ in the index – the big 5 technology companies are reduced to just a 1% weight (5 stocks out of 500). The Equal Weight Index returned just +5.08% to June 30.

Like politics, things aren’t always as equal as they look.

Dividends didn’t help. In fact, they hurt. These are the market’s plodding giants, but the market wants fast growth right now.

Interest rates didn’t help either. Remember when the experts expected up to seven rate cuts in 2024 from the U.S. Federal Reserve? So far, we've had one – from Canada's central bank, but none from the U.S.

The experts now expect one. Maybe.

Soft Landing – So far

The Canadian economy is clearly decelerating, which could result in up to two more rate cuts in Canada. It is a mixed blessing, though. Lower rates help borrowers – and many are strangling on their mortgage rates – but they are also a symptom that the economy is weak.

You don’t push on the accelerator unless you want or need to go faster. Sometimes all you do is spin your wheels.

The U.S. economy is also beginning to stall. Unemployment is rising and more real estate is going into foreclosure.

The Middle East is not cooling down, and Ukraine feels more like a stalemate than a win or loss.

Election Year Trend

A U.S. election year is generally good for markets. There is often a drop in the spring due to polling uncertainty, followed by a later rally once the market figures out the eventual winner.

2024 skipped the spring decline and is ahead of where we would normally be.

The U.S. election playbook has now been torn to pieces. President Biden is now unlikely to be the Democratic candidate in November, so the world is bracing for the return of an erratic president or the inauguration of someone new and unknown. The election cycle could be turned on its ear this year.

What’s Ahead

Despite all the angst, interest rates are likely to come down and the election will be resolved, one way or another. As shown above, election years are typically decent in terms of returns.

While valuations are high in the technology stocks, look again at how poorly the Dividend Aristocrats have done:

S&P 500 +15.29%

S&P Dividend Aristocrats + 2.18%

S&P/TSX + 6.05%

S&P/TSX Dividend Aristocrats + 3.23%

These are the largest and safest of the world’s companies, enterprises that have withstood wars and recessions over the decades. With dividend yields between 4% and 7%, this is where the bargains lie today.

And where we are actively looking.

The Everything List

A client had a problem last month. Her husband made her a list years ago of all their assets and account numbers so that if he fell off a ladder or got swallowed by a whale, she’d know where everything was.

That was ten years ago. “Things change,” she reminded him. “Like your wardrobe, the list is out of date.”

After fruitless entreaties, she finally demanded it as a birthday present. Get it done by then, or else. You know the saying about the mechanic’s car being the one that never starts, and the shoemaker’s shoes that have the largest holes?

He made a new list. Or, rather, I made a new list. The client is my wife. Even though I counsel people to maintain such a list, this financial advisor’s was hopelessly out of date.

How do you make a comprehensive list, and what should you write down?

Fortunately, Raymond James solved this with its Estate Planning Reference Guide. It is a booklet you fill out with spaces for:

- Your Last Will and Testament location

- Financial accounts

- Passwords

- Utility providers

- Instructions to executors and next-of-kin.

Yes, it involves some work, but those you leave behind will bless you for having everything in one place.

Contact us by phone or e-mail and we will be happy to send you your own Estate Planning Reference Guide.

Make it your summer project.

![]()