Our Aging World

Written by Paul Siluch

May 23rd, 2024

Know Thyself

My wife and I just returned from Spain and Portugal where we walked the final 100km of the Portuguese Camino trail. This is one of the historic pilgrim routes to the cathedral at Santiago de Compostella in Spain, a church built to honour the apostle St. James. Approximately 440,000 pilgrims walked all or part of one of the 13 Camino routes in 2023, which is 1,200 pilgrims per day entering the city.

The final point, the cathedral square, is a very busy place.

Most people participate to enjoy the walk, although surveys say 45% of walkers are there for religious, spiritual, or health reasons. As hikes go, it was relatively easy, although consecutive days of 20+ kilometres do take their toll.

Two observations about the walk.

First, while we have been to Europe many times, this time I felt relatively poor. Not poor like we had to stay in hostels, but poor as in “wow, that was more expensive than I remember.”

Inflation has gripped Europe just as it has squeezed Canada. Labour, fuel, and commodities are more expensive, which means meals and living expenses are as well. Canadians used to be able to point at European gas and diesel prices with a smile because ours were so much lower.

Not anymore. Carbon taxes, tighter fuel supplies due to shrinking refinery outputs, plus a host of other factors mean regular gasoline in Victoria now costs exactly what it does in Spain. That was a surprise.

And we used to smirk at European tax rates, especially those in the Nordic countries. Sure, they have great social benefits, but they pay dearly for them. As with gasoline prices, Canada has caught up. Our highest marginal tax rate is now comparable (source: Wikipedia):

Norway 46.4%

Spain 47%

Germany 47.475%

France 49%

Sweden 52%

Denmark 52.07%

Canada 54%

Belgium 60.45%

Portugal 64%

Second, we live in an aging world. It was hard to find pilgrims with hair colour other than grey on the Camino. We walked 100km in 5 days, and the entire 800km of the longest Camino trail can take five weeks. It is mainly retirees with that kind of time, and those walking for health or in memory of a loved one are probably seniors.

It was a visual reminder that we live in an aging world.

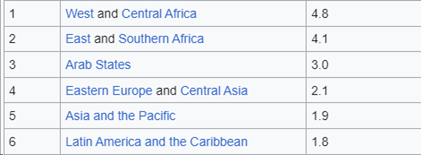

Globally, the world needs 2.3 babies born to every woman to sustain its current population. The number is lower for developed countries because mortality is lower where incomes are higher – 2.1 babies per woman.

The world is right at a 2.3 birth rate today, with population growth coming from the Middle East and Africa while it shrinks everywhere else.

Source: Wikipedia

Why are birth rates falling?

There are a variety of factors, but most of them relate to prosperity. The average British woman in the year 1800 had 5 children compared to 1.6 today (source: Statista). China has only recently followed the same curve, albeit with the heavy hand of government and its One Child policy. Regardless, China has brought more people out of poverty in the last 30 years than any nation on Earth. Its birthrate is now just 1.2 per woman.

Even India, home to one of the youngest populations on the planet, now has an average birthrate of just 2.0. We will be talking about India aging and shrinking in the decades ahead.

The U.S. birth rate is 1.7 babies per female and Canada is 1.5. Both countries rely on immigration to grow.

Nothing is permanent and everything seems to move in cycles. Perhaps with an AI productivity boom, we won’t need as many people. Or, if Elon Musk is correct and we spread to a second planet, we will see birth rates rise to fill the new land. Or there even may be new methods of artificial birth, but that is pure science fiction today.

For now, families are smaller as children are delayed due to choice or economics. It is a global phenomenon and one investors must prepare for.

Investing in an Aging World

Aside from investing in retirement homes and cruise ships, an aging population may also mean higher inflation is here to stay, because:

- There are fewer young workers producing

- And more older people consuming

For example, care homes and in-home care services struggle with finding workers to look after our aging population. It is hard work with no benefits, around-the-clock hours, and we only want to pay minimum wage. That will change.

Government payments to the elderly, whether through pension like Old Age Security in Canada and Social Security in the U.S. are going straight up alongside health care spending. This has resulted in outsized deficit spending that increases every year.

Some government expenses you can cut, but not pensions and health care. This leads to worries about long-term government bonds and how they will be repaid. If they will be repaid.

It is not all doom and gloom, of course. Investors have a wide array of rising investment areas, such as spending on electric power and transmission, artificial intelligence technology, and new health care solutions. These will need funding. However, they will also have to compete with governments borrowing more every day.

What some money managers are doing today:

- Keeping bond investments short – in the one- to five-year range. 30-year bonds look more and more risky.

- Commodities, from gold to copper to energy, are attractive. Few portfolios own them today. The world is short everything from uranium to cocoa these days.

- International managers are investing more in countries with large populations of younger workers, such as India, Indonesia, Mexico, and Saudi Arabia.

You may not be religious, but the Camino pilgrimage is a wonderful place to contemplate and meditate as you walk through some spectacular countryside.

Value Investing in an Overvalued World

There are many philosophies to making money. Some investors put all their money into one basket and watch that basket. Others put money into hundreds of securities so they don’t have to worry about one not working out.

Some investors seek companies growing at extreme rates. This can work but is like juggling hot potatoes. Some seek distressed companies that are worth more if you closed them us and cashed out their assets. This can also work, as long as there is a buyer for those distressed assets.

Our preference – and it isn’t everyone’s preference – is to lean toward the value side of the ledger.

Undervalued stocks. If we can find them.

Everything we buy is just a little hated by investors. If it is loved, it is expensive. We prefer cheap over expensive.

For example, our recent stock purchases have included Nintendo, the video game maker. It is years late in delivering an updated game console. It is coming, but not until next year.

And Nintendo is in Japan, which is a bit of an investment backwater for global investors these days.

As a result, the stock sells for just 6x earnings with a 3% dividend. It has risen 30% since our purchase, making it a ‘single’ rather than a ‘home run’.

We hope for more.

We also purchased Saputo, the Canadian cheese and dairy producer. Cheese is hardly computer chips - as unsexy a sector as you can find. The company expanded in the U.S. and overpaid. It just announced a new CEO.

Everyone likes cheese, right? It doesn’t go out of style. The stock up just 5% for us so far and we like what we see.

Last week, we started a position in Pfizer, the drug company famous for its Covid-19 vaccine and Viagra. Pfizer is a controversial company. Many people now despise vaccines because of the rapid and heavy-handed rollout. Pfizer made close to $30 billion in extra profits from its Covid-19 vaccines and treatments, which saw the shares double in price.

Since then? Cut in half. Vaccine profits have vanished now that the pandemic has passed, and the stock declined from $60 to $28 today.

Unnoticed by most investors is what they did with all the vaccine profits. They purchased Seagen, a leader in cancer therapies, for $43 billion. Pfizer will start rolling out new drugs over the next few years.

The current cancer juggernaut is Merck. The company introduced Keytruda in 2016, its blockbuster cancer drug, but it took over a year to get rolling. Today, Keytruda is one of the most successful drugs in history. Merck stock has tripled in price and the dividend increased eight times.

This could happen to Pfizer, if enough things go right.

At just 12x earnings (when the market sells for double that) and a 6% dividend, very little good news is priced in.

![]()