Evolve or Die

Written by Paul Siluch

February 7th, 2024

“What’s Dangerous is Not to Evolve.”

- Jeff Bezos

In nature, some species thrive while others die off. Why one and not the other? Maybe one adapts to a changed environment while another benefits from dumb luck. Both work.

Ask the dinosaurs. They were bigger than every other life form on Earth and dominated almost every niche above ground. Along came a meteor and suddenly small and burrowing creatures became dominant in a very short space of time. Flying dinosaurs adapted and became birds. No other dinosaurs made it.

Companies are no different. They can prosper for decades and then fall apart when business conditions change, and new competitors arise. It can be sudden, like Blockbuster Video that only survived for 25 years. Or it can be a long decline, like Sears Roebuck that lasted 125 years.

Sears’ demise seems inevitable today. It didn’t have to be. At least, not all of it.

Sears Roebuck began business in 1893 with a mail-order catalogue featuring thousands of products in a 322-page catalogue. It offered lower prices and greater variety to rural America who, until the Sears catalogue arrived on their porch steps, had only local general stores to buy from.

Sears pioneered truck delivery and credit to the masses and the catalogue was so successful, it didn’t open its first department store until 1925.

The catalogue grew to over 100,000 items by the 1950s. Sears expanded into insurance with Allstate in 1931 and started the Discover credit card in 1985. Its brands Kenmore, Craftsman, and DieHard became #1 lines across the country.

The famous Sears catalogue which was, in its way, the internet equivalent of the early 1900s. You looked up what you wanted, ordered it, and it arrived by truck. Doesn’t sound much different than Amazon today, does it?

It was everywhere and everything. And yet still it failed.

Sears Roebuck was like a battleship. By the 1950s, its catalogue offered over 100,000 items. But this battleship was slowly taking on water. Many think it was Amazon that sunk Sears, but the holes in the hull appeared years before.

Wal-Mart, a cost-focussed competitor out of rural Arkansas appeared in 1962. It ate away at the bottom tier of shoppers and forced Sears Roebuck to go upscale. Specialty retailers like Toys “R” Us and Home Depot chipped away sales from general department stores.

The early warning signs for retail were there - competitors like K-Mart and Bon Marche began to fail. Wal-Mart passed Sears in gross sales in 1990 and forced Sears to close its famous catalogue in 1993.

Northern Strength

Not all of Sears was in such dire straits. Sears Canada was formed in 1953 when Sears Roebuck partnered with Simpsons to form Simpsons-Sears. This became Sears Canada in the 1970s when the Simpsons portion was bought out.

Canada is a different market than the U.S. We are a country of small communities spread far apart. Sears Roebuck closed their catalogue operation in the 1993 because so many malls had been built, everyone could drive to one. With far fewer malls, Sears Canada marketed to all income classes in Canada and leveraged its catalogue to reach every corner of this vast underpopulated country.

Sears Canada kept its catalogue. It remained profitable. The company’s wide network of 900 small catalogue stores from Kitimat B.C. to Corner Brook, Newfoundland was almost impossible for any other company to compete with.

I worked at Sears Canada for several summers in the 1970s and it truly was where Canada shopped. The famous promise “Satisfaction guaranteed, or your money refunded” drew people back year after year.

I remember going up to the ski hill in my new matching Sears snow jacket and pants only to see six other people in exactly the same outfit. The same thing happened at the beginning of every school year with new clothes.

That was Canada in the 1970s. Every family shopped from the Sears catalogue.

When the internet arrived, Sears Canada should have been a trailblazer. They put the catalogue on the web, but it was awkward. It held limited items – as few as 500, some records say. On-line retailers like eBay and Amazon listed tens of thousands of items and brands on interactive pages while Sears Canada’s site looked like, well, a catalogue.

The department store format also began to struggle up here. Woodward’s and Eaton’s – two of the Big Four department store chains - vanished. Sleep Country stole the mattress business from Sears Canada and Canadian Tire took the automotive and hardware crowns. Sears Canada soon killed off sporting goods and toys.

But Sears Canada fought back with Sears Home, its own specialty format. And it had still had those 900 catalogue pick-up locations across Canada. These, distribution warehouses and a fleet of trucks were perfect for the new trend towards “on-line” shopping.

Sears Canada could have made it. It had money and forward-looking management. At one point, Sears Canada’s digital sales were larger than those of Wal-Mart. At this point, though, its evolution hit a wall. It had its own “meteorite moment” in the form of a greedy parent down south.

Eddie Lampert was an American hedge fund manager. Seeing value in failing retail brands, he took control of K-Mart and forced a merger with Sears Roebuck. Would two dinosaurs survive better than one? He used most of the new Sears Holdings cash to buy shares to prop up the price. This starved it of working capital and sales slid year after year.

Mr. Lampert looked around for other pockets to pick and spotted the Canadian arm. As the majority owner of Sears Canada, Lampert stripped over $600 million in cash in special dividends – cash intended for the on-line business.

He ended up destroying both the U.S. and Canadian arms of Sears. The crown jewel brands of Kenmore, DieHard, and Craftsman were auctioned off, followed by its real estate. Sears Canada folded in 2017.

Companies that reinvest profits in research, people, and customer service have a good chance of prospering year after year. Just think of Apple Computer or Starbucks.

It is no guarantee, however. Blockbuster Video ran into an unforeseen new competitor called Netflix and even Wal-Mart is struggling against Amazon today.

Sears Canada should have survived. It didn’t.

Constant Change

“Some people don't like change, but you need to embrace change if the alternative is disaster.”

- Elon Musk

Sears expected things to continue forever. They were mostly correct - people will always shop. But they missed that we would shop differently than we used to. Almost all retailers are struggling to adapt to on-line competition where the store, essentially, comes to you.

Some industries have change ingrained in their DNA. They evolve non-stop because they have to. An example of this in our portfolios is pharmaceutical companies. These companies invent drugs that are protected by 20-year patents, which are really just 10 years after development and testing. Ten years is barely enough time to earn back your investment.

AbbVie is a pharmaceutical company in our portfolios. AbbVie’s Humira drug has generated over $200 billion in cumulative sales and may be the most successful drug of all time. Humira reduces inflammation and is extremely effective for rheumatoid arthritis, as well as for psoriasis and Crohn’s disease. It is truly a wonder drug for tens of thousands of people and has made billions for AbbVie.

The problem – and the problem for all drugs – is the short patent life. Humira’s patent window is now over, meaning it can now be made by any company. Humira sales fell over 40% in the last year as competitive versions appeared and prices fell.

AbbVie has a big hole to fill. They must constantly spend on research to reinvent themselves even as Humira sales decline. Many drug companies fail when their blockbuster cow stops giving milk.

AbbVie is filling the hole.

The company came up with two new drugs that are improvements on Humira and more targeted.

- Skyrizi is for psoriasis and Crohn’s disease.

- Rinvoq is for inflammation.

Combined, these two new drugs generated all the lost annual revenue from Humira in 2023.

AbbVie also owns the cosmetic drug Botox. Botox sales suffered during the pandemic. Who needs a shot for wrinkles when Zoom can touch up your appearance on the screen? With people meeting face-to-face again, Botox sales are growing again.

AbbVie shares are +10% so far in 2024, thanks to its successful evolution from older to newer drug. Companies like AbbVie can be mispriced when they are changing. We call these “value with a catalyst” stocks and are ones we look for.

Conversely, companies like Sears are “value traps” – they look cheap but are cheap for a reason. We try to avoid those.

It isn’t easy.

Premature Jubilation

The market’s exuberance is facing a test right now. Around November 1st of last year, the U.S. Federal Reserve signaled that rate hikes were done and 2024 could see interest rate cuts. Markets went crazy. Investors built in 6-7 cuts when the Fed explicitly stated only three were likely.

It is February now and the economy in the U.S. looks better than expected. Jobs are still plentiful (although many are part-time) and manufacturing is picking up. Canada is weaker, but if our neighbour prospers, we usually do too.

But stocks and bonds are now starting to realize that the Fed might not have been kidding. We may only get three rate cuts this year. There might be a hangover in our future. Or at least a minor headache.

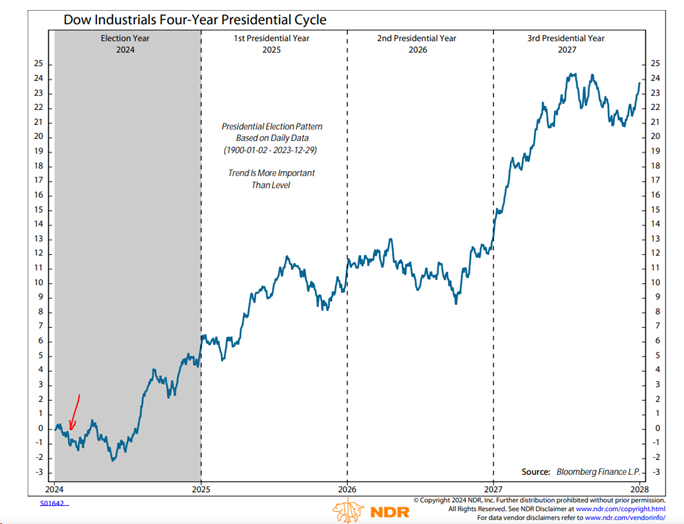

In election years, markets often stumble to begin the year then finish strongly. The U.S. Presidential race this fall will be bitterly contested, but then many have been since 1900 when this data starts.

The red arrow shows where we are right now in the calendar and how the most recent years lined up with the graph.

The pattern is slow start, strong finish over 123 years and 30 U.S. elections.

| Year | 2024 | 2021 | 2022 | 2023 |

| S&P 500 | ? | +25.7% | -19.4% | +26.4% |

As we brace for another contentious election, history reminds us: markets survive politics.

![]()